Why Floating Rate Private Credit Wins in a High-Rate World Most fixed income portfolios are still built for the last regime. They hold assets that lose value when…

Why Floating Rate Private Credit Wins in a High-Rate World

Most fixed income portfolios are still built for the last regime.

They hold assets that lose value when rates rise, then spend time and fees trying to hedge the very risk they hard-wired into the allocation.

Floating rate private credit is designed differently.

In a high-rate environment, it doesn’t just survive rate moves. Its yield is built to move with them.

This article unpacks what that means, how it differs from traditional bonds, and why sophisticated investors are reframing rising rates as a design choice rather than a problem.

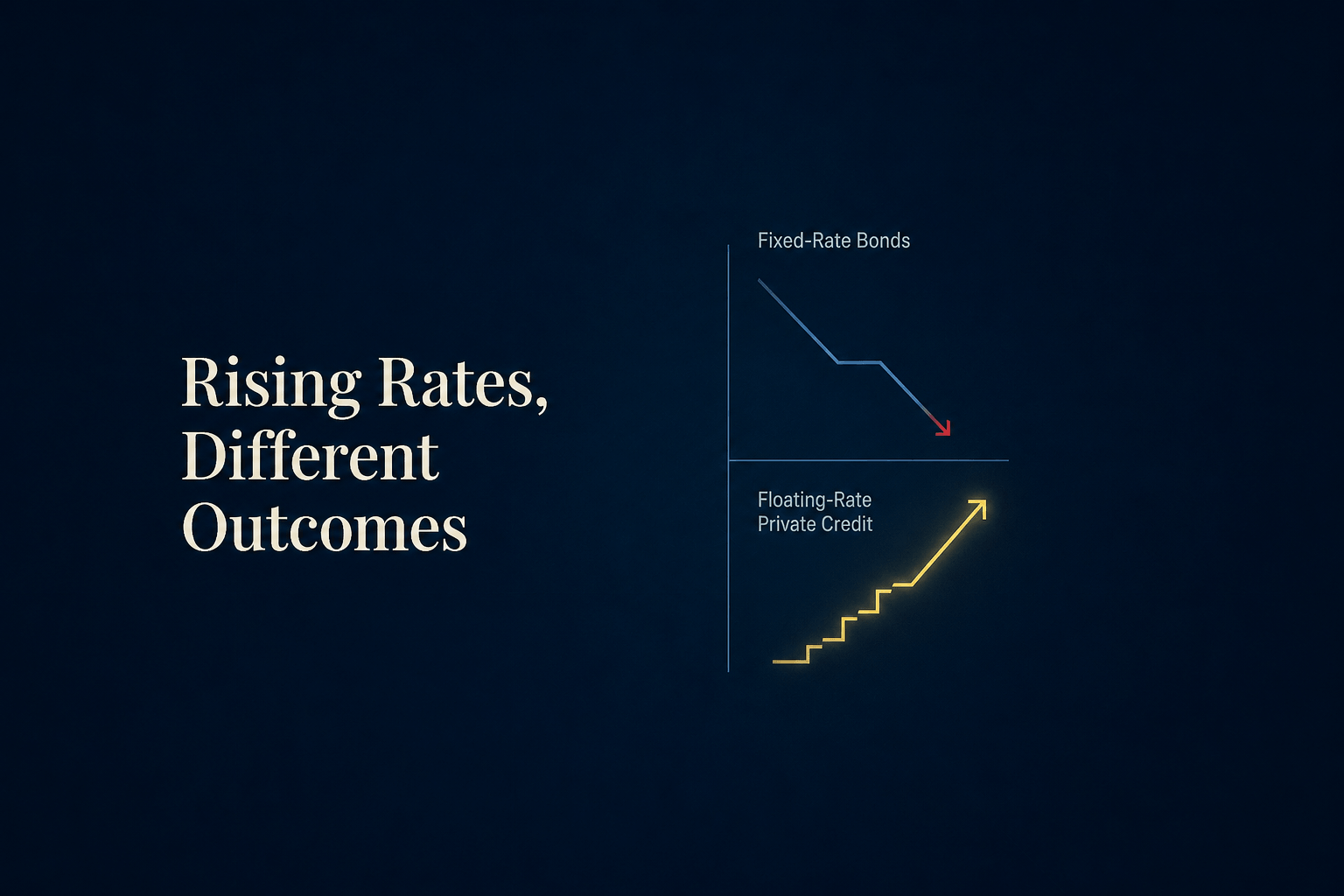

The Problem: Traditional Bonds Are Designed to Suffer When Rates Rise

Most accredited and institutional investors understand the theory. But in practice, fixed income allocations still behave like rate trade victims.

How duration amplifies pain in public bonds

Public bonds are usually fixed-rate instruments. You lock in a coupon on day one. When prevailing interest rates rise:

- New bonds come to market with higher coupons.

- Existing bonds with lower coupons must fall in price to stay competitive.

- The longer the duration, the more their price has to adjust.

The result: the part of the portfolio meant to be “defensive” bleeds when the rate regime shifts.

That’s exactly what investors experienced as central banks moved off zero and repriced the entire curve.

Why “rate risk” is still the dominant risk in many portfolios

Look through a typical fixed income allocation:

- Core bond funds

- Aggregate bond indices

- Long-duration sovereigns or high‑grade corporates

These exposures are often dominated by interest rate risk, not credit risk. The portfolio is implicitly betting that:

- Rates will be stable or lower, and

- Duration will be rewarded.

In a world where policy rates reset higher and stay there longer, that design is misaligned with reality. The portfolio is built to lose when the regime breaks.

What Floating Rate Private Credit Actually Is

Floating rate private credit takes a different approach to the coupon itself.

Floating vs fixed: how coupons reset

Instead of paying a fixed coupon for the life of the instrument, floating rate loans typically pay:

Benchmark rate (for example, a short-term reference rate) + a negotiated spread

As the benchmark rate moves, the coupon resets.

When rates rise, the coupon paid to the lender generally rises with them. When rates fall, the coupon resets lower.

That simple structural difference changes how the asset behaves through cycles:

- You are less exposed to price losses from rate hikes.

- You are more directly exposed to the level of short-term rates through income.

Where floating rate private credit sits in the capital stack

Private credit typically finances companies through senior secured or unitranche loans, negotiated directly rather than issued into a public market.

Key distinctions versus public bonds:

- Terms are privately negotiated, not set by a broad syndicate.

- Documentation can be tighter, with bespoke covenants and structures.

- Pricing can reflect complex, non-commoditized risk, not just index membership.

In that context, a floating rate structure aligns the lender’s income stream with the prevailing rate environment while the private nature of the deal aligns economics with specific risk.

Why Floating Rate Private Credit Is Structurally Advantaged in a High-Rate Environment

In the current regime, the difference between fixed and floating is not academic. It’s economic.

Rising rates: headwind for bonds, tailwind for private credit lenders

Consider two simplified exposures:

- Fixed-rate public bond

- Coupon: locked on day one

- When rates rise: price falls, yield modestly adjusts through capital loss

- Floating rate private loan

- Coupon: benchmark + spread

- When rates rise: coupon resets higher, income increases, price impact is typically more muted from the rate move itself

Both feel the same macro headline — “rates are higher” — but the mechanics are inverted:

- Rising rates hurt fixed-rate bonds because their locked coupon is less attractive.

- Rising rates pay floating rate private credit lenders more as coupons reset.

In other words, the same macro risk many portfolios are still defending against is the one floating rate private credit is specifically set up to monetize.

When the macro risk you fear is the risk you can get paid for

Most portfolios still treat interest rate risk as something to hedge, offset, or dilute.

Floating rate private credit treats it as a design variable:

- If the regime is high-rate and sticky, your income adapts.

- If the regime shifts, your exposure resets with it.

This doesn’t remove credit risk or the need for underwriting discipline. It does, however, remove the contradiction of:

- Fearing rate hikes, while

- Owning assets whose structure is built to be harmed by those hikes.

In a high-rate environment, that contradiction is expensive.

Rethinking Fixed Income: Designing Exposure That Floats With the Regime

For macro-aware allocators, the question is no longer “How do I survive rising rates?” It’s:

“Why am I still holding rate-sensitive assets that don’t float?”

From “rate victim” to “rate participant”

Reframing the problem leads to different portfolio construction choices:

- Less reliance on long-duration fixed-rate instruments as the default “safe” allocation.

- More deliberate use of floating rate structures where the coupon, not the price, does the adjusting.

- Greater emphasis on credit underwriting and manager selection rather than blind duration exposure.

The objective is not to abandon bonds. It’s to recognize that in this regime, part of the fixed income stack should be structurally aligned with how rates actually behave.

Floating rate private credit is one way to express that alignment.

Questions sophisticated allocators should be asking now

If you’re an accredited or institutional investor, a few practical questions follow:

- What percentage of my fixed income exposure loses value when rates move higher?

- How much of my portfolio’s risk budget is implicitly rate risk, versus credit and structural risk where I can be paid more for complexity?

- Where could floating rate private credit replace or complement traditional bond exposures without sacrificing income?

The answers will differ by mandate. The common thread: structure matters more than label.

Where Floating Rate Private Credit Fits for Operators and Macro-Aware Investors

For operators, CIOs, and macro-driven investors, floating rate private credit is not just a yield source. It’s an expression of how you think about regimes.

Why operators and macro thinkers gravitate to floating structures

Operators live in floating worlds:

- Revenues move with cycles.

- Input costs adjust with markets.

- Financing terms reset with conditions.

A capital structure that floats with the environment is more intuitive than one that assumes a static rate backdrop.

For macro-aware investors, floating rate private credit offers:

- A way to participate in higher rates via income rather than fight them via hedges.

- Exposure where documentation, security, and structure are negotiated, not commoditized.

- A lens on how real businesses are funded in a non-zero-rate world.

Using private credit as a deliberate macro expression

Seen this way, allocating to floating rate private credit is not a niche tactic. It is a statement:

- That the post-zero world is not an anomaly.

- That portfolios should be built for structural, not temporary, realities.

- That yield should be earned where the terms, not just the ticker, are understood.

For investors willing to think beyond public bond benchmarks, this is where private markets and macro regimes intersect in a tangible way.

FAQs on Floating Rate Private Credit in a High-Rate Environment

How does floating rate private credit behave when interest rates rise?

Floating rate private credit loans typically reference a short-term benchmark rate plus a spread. As benchmark rates rise, the coupon on these loans resets higher, increasing the lender’s yield. In contrast, the prices of traditional fixed-rate bonds generally fall when rates rise, as their lower fixed coupons become less attractive relative to new issuance.

Why do traditional public bonds lose value in a high-rate environment?

Fixed-rate public bonds lock in a coupon at issuance. When prevailing interest rates rise, new bonds come to market with higher coupons. Existing bonds with lower coupons must trade at a discount to offer comparable yields, which appears as price declines. The longer the duration, the more sensitive the bond is to rate moves.

Is floating rate private credit risk-free in a rising-rate environment?

No. Floating rate structures reduce interest rate risk on the asset’s price, but they do not eliminate credit risk or liquidity risk. Borrower fundamentals, sector dynamics, documentation quality, and manager discipline still matter. The key point is structural: the income side adjusts with rates instead of being fixed against them.

How do sophisticated investors use floating rate private credit in a portfolio?

Institutional and accredited investors often use floating rate private credit as part of their credit and alternative income allocation, particularly when they expect rates to remain elevated or volatile. It can complement or partially replace traditional bond exposure to lower the portfolio’s sensitivity to rate hikes while maintaining, or even enhancing, income potential.

What’s the main difference between floating rate private credit and leveraged loans or public credit ETFs?

Floating rate private credit typically involves directly originated or privately negotiated loans with tailored structures, covenants, and pricing, rather than broadly syndicated loans or public-market instruments. That private, negotiated nature is distinct from owning a pooled, tradable instrument, and it places more weight on manager selection, deal sourcing, and underwriting discipline.

The Manhattan Private Credit View

At Manhattan Private Credit, we see the current environment as a stress test of portfolio design.

If rising rates are hurting your bonds, it’s not just a macro story. It’s a structural choice baked into what you own.

Floating rate private credit takes the other side of that choice. It allows lenders to be paid when rates rise instead of penalized by the same move.

For accredited investors, operators, and macro-aware allocators, that’s the conversation that matters: not just how much yield you see on a factsheet, but how that yield behaves when the regime shifts.

Learn more at manhattanprivatecredit.com.

Most fixed income portfolios are built to lose when rates rise. Floating rate private credit is built to get paid. Because these loans reset with prevailing rates, they can turn a high-rate environment from a portfolio headache into a deliberate design choice rather than a risk you’re constantly defending against.